Return to My Accounts

Return to My Accounts

Return to My Accounts

Return to My Accounts

Long-term care insurance: Is it right for you?

Long-term care insurance can offer flexibility to cover long-term or extended care expenses

Here are answers to some commonly asked questions about long-term care and long-term care insurance coverage to help you determine if it’s a good fit for you.

In this article:

- What is long-term care?

- What is long-term care insurance?

- How does long-term care insurance work?

- Why should I buy long-term care insurance?

- Do I need long-term care insurance?

- When should I buy long-term care insurance?

- How much does long-term care insurance cost?

- How do I choose the best long-term care insurance policy for me?

- Are there other options besides a traditional long-term care insurance policy?

- What if I buy a long-term care policy and don’t end up needing it?

- What are the pros and cons of long-term care insurance?

- Other considerations for long-term care planning

What is long-term care?

Long-term care is a variety of services designed to help those who can no longer care for themselves for extended periods of times. It can offer support to people who need help performing basic activities of daily living (ADLs), such as dressing, bathing and eating due to an illness, injury or aging. It can also help with day-to-day activities like housework, money management and shopping.

There are many types of long-term care options, including varying locations and levels of engagement, depending on your specific needs. This includes:

- In-home services

- Assisted living-facilities

- Adult day care centers

- Hospice long-term care

- Nursing homes long-term care

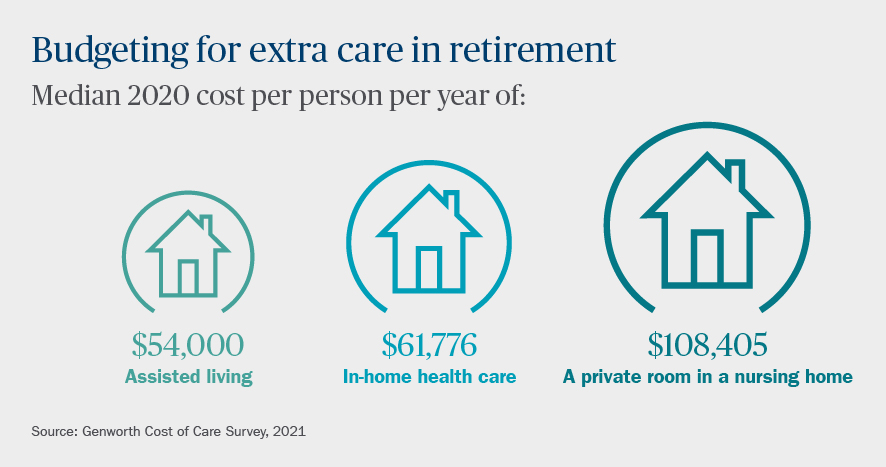

Cost breakdown of long-term care options

If you or a loved one needs more hands-on care, you have choices — including assisted living or home health care. The cost can vary significantly based on the type of care you receive.

What is long-term care insurance?

Long-term care insurance provides you with additional financial support for long-term care needs that are not covered by Medicare, Medicaid or health insurance.

How does long-term care insurance work?

While policies may vary, they typically require you to pay a premium on a consistent basis — whether or not you are currently using long-term care. If you need to use the benefits outlined in your policy, the policy will pay for the type of care detailed in the policy. This payment is usually a certain dollar amount per day and is set for a specific time period.

Usually, a policy determines when benefits are payable based on your ability to perform certain daily tasks. It will also consider the total number of activities of daily living you are unable to perform.

In other instances, policies may require a doctor to deem care medically necessary.

Why should I buy long-term care insurance?

Someone turning age 65 today has almost a 70% chance of needing some type of long-term care services and support in their remaining years, according to the U.S. Department of Health and Human Services.1

Even if you have saved for retirement, it’s important to prepare for unexpected events — and needing long-term care could be one of the costliest of those events. For example, if you need to move to a nursing home, the median cost per year for a private room is more than $108,000.2

Health maintenance organizations (HMOs) Medicare, and Medigap will not cover every heath care expense — and Medicaid may cover some extended care costs, but only under certain limited conditions. As a result, out-of-pocket expenses for long-term care could significantly impact your life savings.

Do I need long-term care insurance?

You’ll want to consider a variety of factors before purchasing long-term care insurance, such as your age and finances. Long-term care insurance may be a good fit for you if some or all the following requirements apply:

- Are between 40 – 84 years old

- Have assets

- Can and will be able to afford long-term care insurance premiums

- Are currently in good health and are considered insurable

Everyone’s situation is unique. Your Ameriprise financial advisor can help you decide if long-term care insurance is a beneficial approach for you.

How much does long-term care insurance cost?

The cost of a long-term care policy depends on a variety of factors, including the size of benefits, length of benefit time, care options and optional riders.

Your premium cost is based primarily on your age at the time of purchasing a long-term care plan. Typically, the younger you are, the lower your monthly premium will be.

You may need to adjust the length of coverage or the daily payment in your policy to make the purchase realistic for you. You may also want to consider a policy that provides automatic cost-of-living increases to protect against inflation.

How do I choose the best long-term care insurance policy for me?

When comparing policies, pay close attention to these common features and provisions:

- Elimination period: The period before the insurance policy will begin paying benefits.

- Duration of benefits: The limitations placed on the benefits you can receive (e.g., a dollar amount such as $150,000 or a time limit such as two years).

- Daily benefit: The amount of coverage you select as your daily benefit, which typically ranges from $50 to $350.

- Inflation rider life insurance: Designed to adjust the dollar amount of your coverage to keep up with rising costs, such as medical care.

- Range of care: Coverage for different levels of care (skilled, intermediate, and/or custodial) in care settings specified in the policy (e.g., nursing home, assisted living facility, at home).

- Pre-existing conditions: The waiting period (e.g., six months) imposed before coverage will go into effect regarding treatment for pre-existing conditions.

- Other exclusions: Whether certain conditions are covered (e.g., Alzheimer's or Parkinson's disease).

- Premium increases: Whether your premiums will increase during the policy period.

- Guaranteed renewability: The opportunity for you to renew the policy and maintain your coverage despite any changes in your health.

- Grace period for late payment: The period during which the policy will remain in effect if you are late paying the premium.

- Return of premium: Return of premium or nonforfeiture benefits if you cancel your policy after paying premiums for several years.

- Prior hospitalization: Whether a hospital stay is required before you can qualify for long-term care insurance benefits.

Are there other options besides a traditional long-term care insurance policy?

Besides a traditional long-term care insurance policy, you could also consider life insurance with a long-term care rider or a hybrid life and long-term care insurance policy.

- Life insurance with a long-term care rider is a living benefit that lets you access a portion of the policy's death benefit to pay for long-term care expenses. If you use your rider's long-term care benefits, your policy's death benefit will go down proportionately. If you don't use your long-term care benefits, your heirs will get the full death benefit from your life insurance policy, minus what you owe on any policy loans.

- With a hybrid life and long-term care insurance policy, emphasis of the benefits is on long term care benefits, with the life insurance secondary. These hybrid insurance policies are typically funded with a single upfront premium and offer the benefits associated with the life policy base, together with additional benefits of long-term care coverage. This policy basically creates a pool of money that can be used to pay for long term care either for a specified minimum period of time, or for a lifetime.

Your Ameriprise financial advisor can help you fully understand the benefits, exclusions and provisions of your preferred long-term care insurance policy.

What if I buy a long-term care policy and don’t end up needing it?

If you’re concerned about spending money on long-term care insurance that you’ll never use, you could consider some of the hybrid long-term care insurance options available. Many life insurance policies now offer a long-term care benefit rider that allows the policyholder to use a portion of the death benefit for long-term care. Additionally, some life and hybrid long-term care insurance policies will pay a death benefit if the policyholder never needs long-term care.

Both options mean that you or your beneficiary may benefit from the policy regardless of your circumstances.

What are the pros and cons of the different types of long-term care insurance?

| Standalone long-term care | Life insurance with a long-term care benefit rider | Hybrid of life insurance and long-term care | |

|---|---|---|---|

| Pros |

|

|

|

| Cons |

|

|

|

Other considerations for long-term care planning

Talk to your family and financial advisor about various care and housing options, the potential involvement of others and the associated costs. For example, if your parents require long-term care, do you anticipate providing financial support for them? If you become injured or ill to the extent that you require full-time assistance, what type of care would you prefer — family members or nursing staff?

In addition, your Ameriprise financial advisor can work with you and your attorney to help you organize and address more complex questions:

- How much money should you set aside for possible long-term care needs? When should you start doing this?

- Have you coordinated long-term care planning with your estate planning needs?

- Have you prepared advanced medical directives?

- Are your important documents and records organized?

An Ameriprise financial advisor can help you make informed choices

An Ameriprise financial advisor can provide guidance as you review policies to help you determine the type and amount of long-term care protection that's right for you.

Or, request an appointment online to speak with an advisor.

At Ameriprise, the financial advice we give each of our clients is personalized, based on your goals and no one else's.

If you know someone who could benefit from a conversation, please refer me.

Background and qualification information is available at FINRA's BrokerCheck website.